The Wall Street Journal recently published a guide to the new tax laws that took effect January 1, 2018. The 80 page guide lays out how the laws will impact most Americans, with an estimated 80% enjoying a tax cut in 2018; 5% (likely not enjoying) a tax increase; and the remaining 15% not seeing a change. Since the New York City real estate market is dependent upon the income of Americans and industries from all over the country, the new tax code is sure to have a ripple effect in Manhattan. Moody’s Analytics predicts that home prices will be between 4-10% lower in the summer of 2019 than they would have been without the tax code changes. Let’s take a look at the changes laid out in The Tax Cuts and Jobs Act to get a sense for what we might expect – I’ve ordered them so that those most likely to impact the NYC real estate market are on the top.

Lower Tax Rates

For most Americans, tax rates have been reduced and income thresholds have been increased. Click here for the full rundown on tax brackets effective January 1, 2018.

Increased Standard Deduction & Repealed Personal Exemptions

Tax returns will be simpler for approximately half of the 47 million Americans who itemized their deductions through 2017. The new standard deduction cap is $24K for married couples (up from $13K) and $12K for singles (up from $6.5K).

Child Tax Credit

Families with children under age 17 may now claim a $2K tax credit per child, up from $1K.

Investment Income Taxes

Rates for long-term capital gains and dividends remain favorable: 0% up to $38.6K for singles/$77.2K for married couples; 15% between $38,601 – $425,800 for singles / $77,201 – $479,000 for couples; and 20% above $425,800 for singles / $479,000 for couples. The 3.8% net investment income surtax remains unchanged.

Revised Alternative Minimum Tax

The AMT exemption has been expanded and analysts predict that the unpopular tax will now only impact 200K returns, down from 5 million.

Estate / Gift Tax Exemptions

The estate tax threshold has been doubled to $11.2M for singles and $22.4 for married couples. This change is expected to reduce the number of estates affected by this tax from 5300 in 2017 to 1,700 in 2018.

State and Local Tax Deductions

The previously unlimited State and Local Tax Deductions (SALT) are now capped at $10K for both singles and married couples, a change that will most impact states with the highest state and local taxes: New York, New Jersey, Connecticut, California, Maryland, and Oregon.

Changes to Mortgage Interest Deductions

New buyers will be able to deduct interest on mortgages up to $750K for a first and second home, down from $1M. This change does not apply to current mortgages.

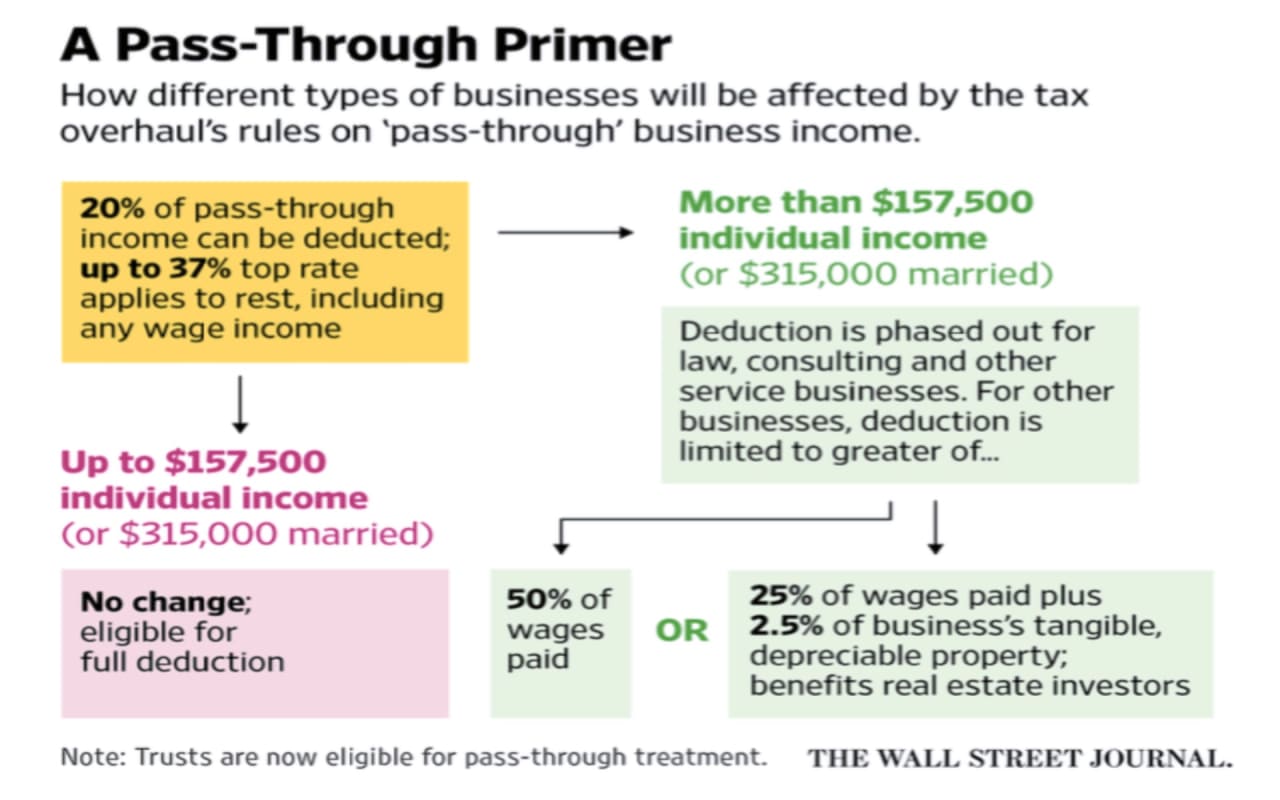

Business Pass-Through Income

20% of net income can now be deducted for qualifying pass-through business owners whose taxable income is below $157,500 for individuals and $315,000 for married couples.

Equipment Purchases

100% of the cost of new and used business equipment can now be written off for the first year, a change from the former tax code in which deductions were divided across several years. This cut applies to purchases made between September 27, 2017 until December 31, 2026, after which deduction amounts will go down each year until 2027, when the tax cut is set to expire. Unfortunately for us, this cut is not applicable to real estate firms.

Business Debt Deductions

For businesses that have grossed at least $25M in the last three years, interest deductions on new and existing business debt will be capped at 30% of earnings before taxes, interest, amortization, and depreciation. After 2022, this limit will apply to earnings before interest and taxes. Not included in this change are car dealers and electric utilities. Farmers and select real estate companies can elect to opt out of the interest cap.

Medical Expense Deduction

The threshold for deduction of medical expenses has been reduced so that those who spend 7.5% of their income (down from 10%) can now deduct those expenses as long as they itemize the deductions.

Alimony Payments

After 2018, alimony payments will no longer be tax deductible for the payee nor taxed as income for the recipient. This could lead those who have to pay alimony to push for lower alimony payment amounts since the payouts will be more expensive as a result of the tax law.

529 Education Accounts

These previously-for-college-only accounts can now allocate up to $10K per year per student towards K-12 private school tuition, and up to $15,000 a year can now be transferred from a 529 plan into a 529 ABLE account, for use by those who became blind or disabled before the age of 26. Rules vary on a state to state basis.

Student Loans

Student loans that are forgiven because of death or disability are no longer taxable.

Repeal of Obamacare Mandate

Beginning in 2019, there will no longer be a penalty for Americans who choose not to pay for health coverage.

As the markets react to the changes, some Americans brace themselves regarding what’s to come, while others suggest this is healthy and that the correction has been a long time coming. Since New York City is still strong in all segments (though weakest in the ultra luxury section), it’s too soon to know how the real estate economy will fare as a result in the coming years. If Moody’s Analytics is correct, it will be good news for buyers looking to get into the New York City market while the price is right.